MREIF Deep Dive: Reshaping Nigeria's Housing Finance Landscape

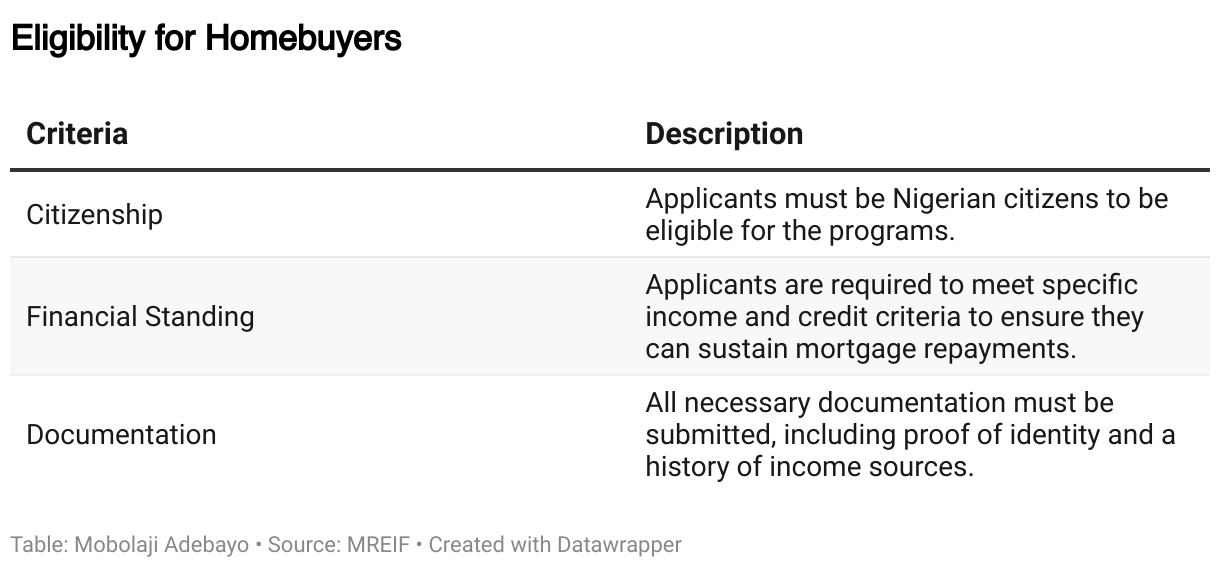

Nigeria's housing sector is caught in a paradox: while there is a vast population in need of homes, the mortgage market remains small. This has left millions of potential homeowners on the sidelines, with mortgage penetration of 5%, a fraction of the required level. Now, a new initiative, the MOFI Real Estate Investment Fund (MREIF), accessible to banks, developers, and homebuyers, has emerged to address this critical gap. Positioned as a credible government-sponsored catalyst, MREIF aims to unlock long-tenor, lower-cost mortgages at scale, providing a new and viable path to homeownership for millions of Nigerians.

For years, Nigeria's mortgage market has been constrained by short tenors, often lasting less than 7 to 10 years, and high nominal interest rates. A typical mortgage rate in Nigeria ranges between 7 and 10 percent for Federal Mortgage Bank of Nigeria (FMBN) and between 15 and 25 percent for commercial mortgage institutions, making it one of the highest in the world. This makes home loans prohibitively expensive. The Nigeria Mortgage Refinance Company (NMRC), while providing some liquidity, has remained modest in scale relative to the nation's housing deficit, which is estimated to be in the tens of millions.

Recent funding announcements signal renewed momentum but are still a fraction of the required investment. The fund has raised a total of ₦250 billion so far through its first and second phases of funding. The initial ₦150 billion was a seed investment from the Federal Government, followed by ₦100 billion fully subscribed by private investors.

MREIF's design is a targeted response to this market failure. Sponsored by the Ministry of Finance Incorporated (MOFI) and managed with private sector partners, its core mandate is a triple-play intervention to tackle the issue from multiple angles:

Demand-Side Affordability: The fund (a N1 trillion programme size with a 99-year life) will provide long-term, lower-cost mortgages (20 years at a fixed interest rate of just 9.75% per annum) directly to qualified buyers.

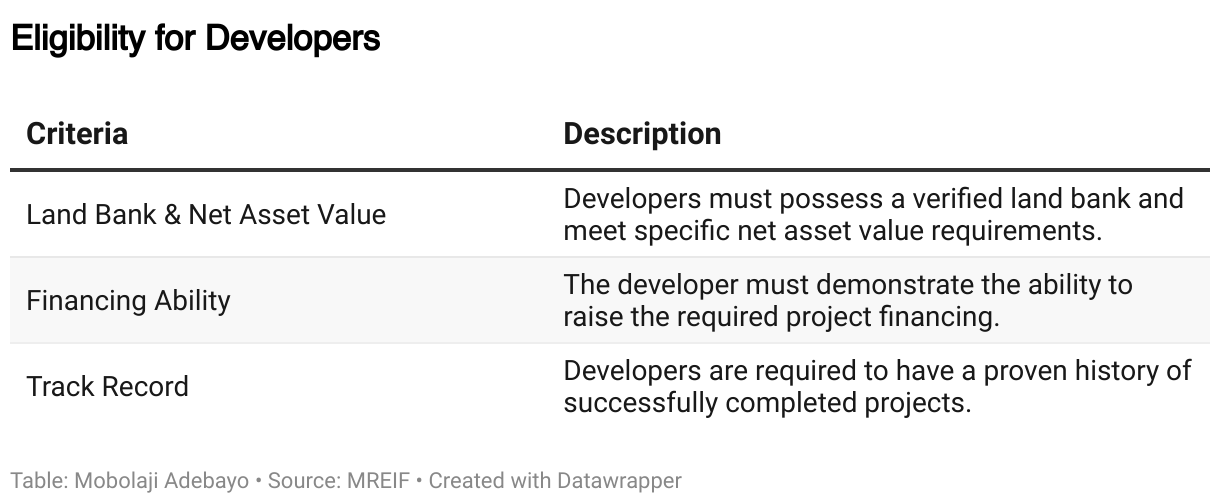

Supply-Side Derisking: It will offer conditional offtake and credit enhancement to developers, stimulating new supply at price points that are accessible for mortgage-eligible buyers.

Capital-Market Flywheel: By creating standardized, bankable pools of mortgages, MREIF will make refinancing more viable for institutional investors like Pension Fund Administrators (PFAs), which will ultimately reduce the long-run cost of funds.

Public communications from the fund reference an ambitious, albeit directional, target to enable the sale of up to 1 million homes over time, underscoring the program’s potential scale. Initial market signals indicate MREIF is gaining momentum. A list of banks that have access to the fund include Access Bank, First City Monument Bank, AG Mortgage Bank, Infinity Trust Mortgage Bank, Union Bank, Providus Bank, HomeBase Mortgage Bank Ltd, and Stanbic IBTC.

However, the fund’s ability to achieve scale hinges on closing three critical execution gaps:

Durable Funding: For MREIF to maintain single-digit pricing, it will require a sustained and substantial inflow of blended or concessional capital.

Friction-Light Title: The complex, costly, and time-consuming process of perfecting property titles is a major bottleneck that erodes affordability. Standardized due diligence and digital records are essential to shave months and hundreds of basis points off effective Annual Percentage Rates (APRs).

Borrower Acquisition: To achieve a step-change in mortgage penetration, the fund must streamline borrower acquisition at scale. This will require integrating with payroll systems and retirement savings accounts (RSAs) to expand the pool of eligible borrowers.

Mitigating Risks for Long-Term Viability

As with any major market intervention, MREIF faces risks, including interest-rate and foreign exchange volatility, execution drift, and concerns about developer quality. Mitigations are being built into the framework: interest-rate caps and refinancing windows to protect affordability, standardized documentation to improve throughput, and escrowed progress payments to manage developer risk.

For a typical salaried buyer, MREIF could transform a short-term, expensive loan into a manageable 20-year commitment with monthly payments that fit their budget. The fund’s ultimate success will serve as a key test for public-private partnerships aiming to solve Nigeria’s housing crisis. The visible momentum suggests commercialisation is well underway, and the next phase of the program will be closely monitored by investors and policymakers alike.